Altius Renewable Royalties: royalties on renewable energy

History

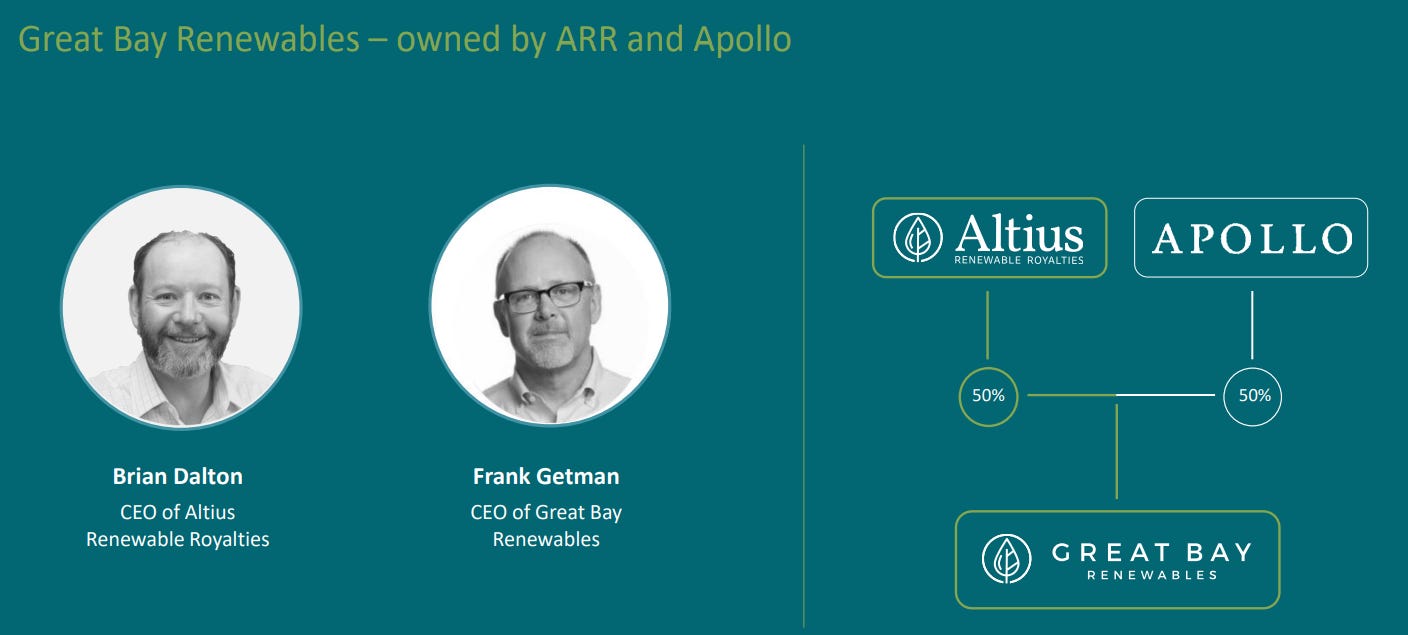

Altius is a spinoff from Altius Minerals (AM), a royalty company with a focus on base metals. AM , among other things, owned some royalties on coal mines. The outlook for coal mines became worse in 2016 when plans were announced to phase out coal production in Canada by 2030. AM then decided to take their revenue from coal and invest it in the energy sources that were going to replace coal in the future, which would be mainly renewable energy. Royalties on renewable energy didn’t exist yet at the time so they searched for partners with the technical knowledge and started to introduce the idea to companies constructing renewable energy projects. They found a partner in Frank Getman, an entrepreneur with experience in developing renewable energy projects. Together AM and Getman created Great Bay Renewables (GBR) in 2017 to explore the possibilities for using royalties in the financing of renewable energy projects. Altius Renewable Royalties (ARR) was formed in 2019 as a division of AM and then they acquired GBR, where Getman was and stayed ceo. After that ARR made a joint venture with Apollo, the private equity company, in October 2020 where Apollo would get a 50% stake in GBR in exchange for an $ 80M investment in GBR. After that $ 80M all new investments would be evenly matched by ARR and Apollo. GBR already had one royalty on a hydro and solar asset in Vermont before ARR acquired the company. After the Apollo deal GBR started to deploy capital mainly through deals with the second and third largest independent renewable energy project developers in the US, APEX Clean Energy and Tri Global Energy (acquired in 2022 by Enbridge). In exchange for investments GBR received royalty deals on a number of projects in development. In 2021 ARR did an IPO at $ 11 per share and Altius Minerals retained 58% of the shares.

What do they do?

Basically, ARR gives developers of renewable energy projects (solar, wind, hydro,…) money to develop their project in exchange for a royalty on the future revenues these projects will generate. The rate can vary, but they typically get between 2.5 and 3% for wind projects and 1.5% for solar projects. It is also important to notice that the royalties run in perpertuity, there is no end date.

Originally ARR looked to finance pre-production stage projects, where it would take a couple of years before they became operational, but after a while they started to notice a shift in the market: in the past developers wanted to hedge out all of their production by locking everything down under long term power purchase agreements; this was ideal for “annuity-like” investors like pension funds who could get predictable returns. But with rising power prices hedging everything doesn’t seem as attractive anymore. So builders now want to have at least a part of their output unhedged, but this alienates their original type of investors, who liked the annuity-like returns. This creates a need for a more “equity-like” type of funding in the capital structure, which creates an opportunity for ARR to step in and provide capital in exchange for a future royalty. This shift also means they are able to fund later stage projects, which gets them royalties sooner. ARR aims for an internal rate of return on their projects of 8-12%, the early stage projects will be closer to the top of that range, the later stage projects will be more in the 8-10% range.

At the moment ARR holds a portfolio of 25 royalties of wich 10 are already producing revenue. The projects are in wind, solar and hydro and combined should generate 15 GW.

An investment in this company, at this stage, is primarily a bet on the jockey, which is the team around Altius Minerals ceo Brian Dalton. Mr Dalton, who is also ceo of ARR, and his team have a good track record as royalty investors in AM in the past 20 years, working anticyclical, being patient and mostly investing when capital was scarce and waiting patiently for years and not making deals when capital was abundant and they couldn’t get good deals. I expect the team to be equally rational and disciplined with ARR and that this strategy will generate good returns for shareholders in the years to come. (Yes, this is the same Altius Minerals that is the main shareholder of Orogen Royalties, which was one of their smart moves in the past.)

Financials & Valuation

All numbers are in Canadian dollars unless otherwise stated

Share price: $ 6.97

Number of shares : 31.4 million

Market capitalization: $ 219 million

Options : 1 M

Cash : $ 56 M

Debt : 0

Enterprise value : $ 163 M

Valuing this company is not easy, because there are a lot of different variables, and they will probably raise more cash in the future and invest it in a lot more projects. But if we just look at their current portfolio, if they don’t invest anything anymore in the coming years (conservative, because they will) they should receive $ 31 M in revenue in about 5 years. I estimate they’ll have around $ 4-5 M in costs by then, so they should be nicely profitable at that time. If I put a realistic multiple on that expected profit and discount it back to today, I arrive at a share price range of between $ 7 and $ 11 for what the company is worth today. They have also indicated that they think their share price is undervalued today, and that they wouldn’t think of raising new capital at these levels. Insiders, who I consider smart investors and who know the company well, bought shares at the IPO at $ 11 and have been buying more shares between $ 7 and $ 10 since then. In December of last year ARR raised an extra $ 35 M at $ 9 per share, and Altius Minerals participated and bougt 2.3 M extra shares.

All this demonstrates that they clearly also think that at the current levels the share price is not reflecting the value of the company.

Risks

The biggest risk is probably government regulation and permitting affecting projects: delaying projects getting build or stopping them from operating. Since increasing energy from renewable sources is a policy goal for the coming years, one would expect that most governments should be cooperative, but there can always be exceptions. The huge increase in renewable projects in the US the past two years, further stimulated by the Inflation Reduction Act, has overwhelmed governments and networks, causing delays in a lot of solar and wind projects, mostly because of interconnection delays. This is also one of the main reasons the share price has come down a lot in the past couple of months, because it also means revenue for ARR on some of those projects has been delayed.

Another risk is that they depend on third parties, if any of their partners gets into financial trouble, then that could affect ARR. In theory barriers to entry in the business are also low, so competition for future projects could increase, which might lower the returns on those projects. For now there are very few companies doing the royalty model on renewable energy projects.

A big part of the cash ARR still has is already committed for further investments in projects. This means that somewhere next year if they want to continue to grow, they will need to find more money. At the current share price raising extra money isn’t an attractive option, and mangement has ruled that out. It remains to be seen if they can find attractive alternative ways to raise money (bank lans, green bonds, …). If not, then they may have to pause their growth until the share price recovers.

Conclusion

ARR is an interesting company with smart management that is pioneering royalty financing in the renewable energy sector. I think management , considering their track record, will build this company in the coming years to a much bigger company than it is today and that ARR can be an interesting long term investment. The share price came down in the past couple of months because of some delays at a couple of projects, and because sentiment for alternative energy stocks has been negative lately, but these are temporary issues, and they make that the stock today looks attractive in a long term perspective.

There is also a free option that, considering its unique profile, it could become a darling of ESG investors, and see its share price rise far above its intrinsic value as all ESG-related funds pile into this name in the future when it gets a bit bigger, but I’m not counting on that for my investment thesis.

*A special thanks to Jeroen Vandamme of the Analyse newsletter (www.analyse.be), who first informed me about the company in his newsletter.

Disclosures / Disclaimers: I own shares of Altius Renewable Royalties. This is not a solicitation to buy, sell, or otherwise transact any stock or its derivatives. Nor should it be construed as an endorsement of any particular investment or opinion of the stock’s current or future price. To be clear, I do not encourage or recommend for anyone to follow my lead on this or any other stocks, since I may enter, exit, or reverse a position at any time without notice, regardless of the facts or perceived implications of this article. I am not a financial advisor. Please do your own due diligence.