Since it was Oscar week, this week I bring a new interesting stock from the movie world, enjoy!

History

Kinepolis was founded in 1968 when the Bert family opened a small cinema in Belgium. In 1997 they merged with another Belgian group and Kinepolis Group was born. In the decades after that (mostly since 2014) they opened numerous new cinemas and did a number of acquisitions, making Kinepolis a group that today has 110 locations (1162 screens) in 9 countries in Western Europe and North America.

What do they do?

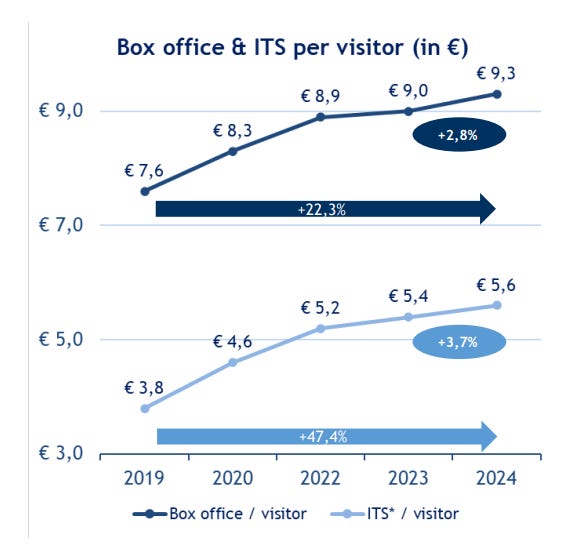

Kinepolis is one of the best operators in their sector. One of the reasons for that is that since Eddy Duquenne became ceo in 2008 (first external ceo), he installed a culture of constantly looking for small improvements. Every year management and personnel have to come up with new ideas to compensate for a potential 5% drop in visitors (which would give a roughly 12% drop in EBITDA because of the relatively high fixed costs). In the first years this mainly led to ideas to cut costs and increase efficiency, but in the past decade the mix has shifted more to ideas to increase revenue. Every year they now get 300 to 400 potential ideas from their personnel they can work with. One of the things Kinepolis also does well is innovate: in the past they have introduced an number of concepts which allow them to charge more for a ticket (‘premiumization’): Cosy seats (two seats with a table), LaserULTRA (better sound and sharper images), ScreenX (two extra screens on the left and right side for a more immersive experience), movies in 3D and 4D,… This way they could increase the average ticket price paid year after year.

The In Theatre Sales (snacks and drinks) also increased with more than inflation in the past years due to several ideas to boost sales: in the last five years in-theatre sales per visitor went up from € 3.8 to € 5.6.

All these things make Kinepolis one of the best operators in the business, which makes them more profitable than most of their peers, and they use the cashflow they produce to acquire competitors. This led to big growth in 2013-2019, when they acquired a number of competitors and went from 23 to 109 cinemas through M&A. Once they acquire a competitor, they gradually introduce their successful concepts in those cinemas and usually manage to significantly raise their profit margins within the first two years.

Financials & Valuation

All numbers are in euros, unless otherwise indicated

Euronext Brussels: KIN

Share price: € 33.40

Number of shares: 26.7 M

Options: 0.6 M

Number of shares fully diluted: 27.3 M

Market cap: € 892 M

Cash: € 84.6 M

Debt: € 403.9 M (excl. IFRS 16)

Enterprise value: € 1211 M

Kinepolis had a period of good growth between 2013 and 2019, fueled by acquisitions: revenues went from € 246 M to € 552 M and earnings per share increased from € 1.38 to € 2.18 but then came COVID and they had to close their cinemas, which led to losses and an increase in the debt in 2020-2021. From 2021 the results started to recover and in 2023 they were back to the levels from 2019. Unfortunately the strike in the second half of 2023 in Hollywood by writers and actors caused a number of blockbusters that were planned for 2024 to get delayed or cancelled, which caused a weak movie offering with few blockbusters in 2024: visitor numbers dropped 8%, which led to 4.5% lower revenues, 11% lower adjusted EBITDA and a 28% drop in adjusted earnings per share from € 2.15 to € 1.56.

The low number of blockbusters in 2024 was exceptional, and things should normalize in 2025, with a good line up expected. This means earnings per share should recover and surpass the 2023 numbers again. I think they can get to around € 2.4-2.5 as they further roll out their premiumization initiatives in their North-American cinemas to increase margins there.

The net debt (excluding IFRS 16) was also further reduced last year to € 319 M (-15%) and is now again below two times adjusted EBITDA. This gives Kinepolis again more room for new acquisitions which could boost sales and earnings in the coming years. It won’t be a straight line, and it will depend on the timing and size of the acquisitions, but I think Kinepolis should be able to increase earnings per share by double digits (>10%) on average in the next decade.

The share price has gone down more than 20% over the past year and is now trading at roughly 13 times my estimate for this year’s profit, which seems too low considering the company’s potential in the coming years.

Risks

One of the main risks is that they depend each year on the movie line up that the Hollywood studios and others provide. Ceo Duquenne has often referred to this as Kinepolis being like a restaurant that has no control over what’s on the menu. If it’s a weak year, or potential blockbusters disappoint, then visitor numbers will go down and Kinepolis will make less money. They don’t have much control over this, and it can cause volatility in their results from one year to another.

The weather is also a volatile factor that influences visitor numbers.

A new pandemic in the coming years could again force Kinepolis to close its cinemas and suffer losses.

In general there are alternatives to cinemas that are competition for Kinepolis: streaming services like Netflix are obvious ones. If streaming becomes more popular, this could weigh on visitor numbers in the future. They counter the threat of these alternatives by trying to make going to the movies a special experience that you can’t copy in your own home. So far this has worked relatively well, but there’s no guarantee that this won’t change in the future.

Conclusion

Kinepolis is one of the best players in its sector, that’s had a couple of tough years because of COVID and the Hollywood strike, but I think that period is now behind them. In the coming years they can focus again on further consolidating the sector by acquiring weaker competitors and improving their profitability after the acquisition. This way I think they still have several years of growth ahead of them, even if the industry itself is not growing, and even slightly contracting every year.

Disclosures / Disclaimers: I own shares of Kinepolis. This is not a solicitation to buy or sell any stock. To be clear, I do not recommend for anyone to follow my lead on this or any other stocks, since I may enter, exit, or reverse a position at any time without notice, regardless of the perceived implications of this article. I am not a financial advisor. Please do your own due diligence.